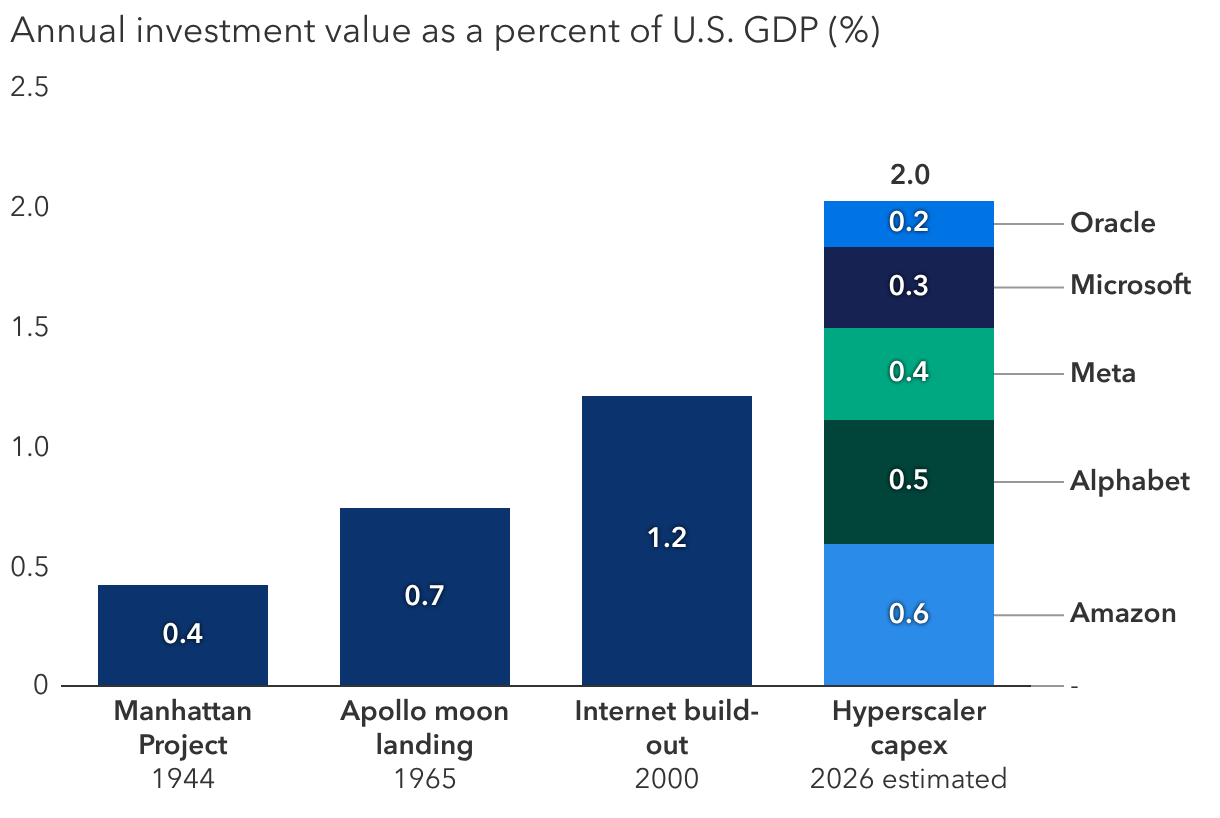

The debate over artificial intelligence has taken a turn so sharp that it could strain your neck. Initial exuberance over AI’s transformative potential sparked investor fears of an AI bubble. But that concern has now been overshadowed by anxiety that the AI juggernaut will steamroll large segments of the global economy.

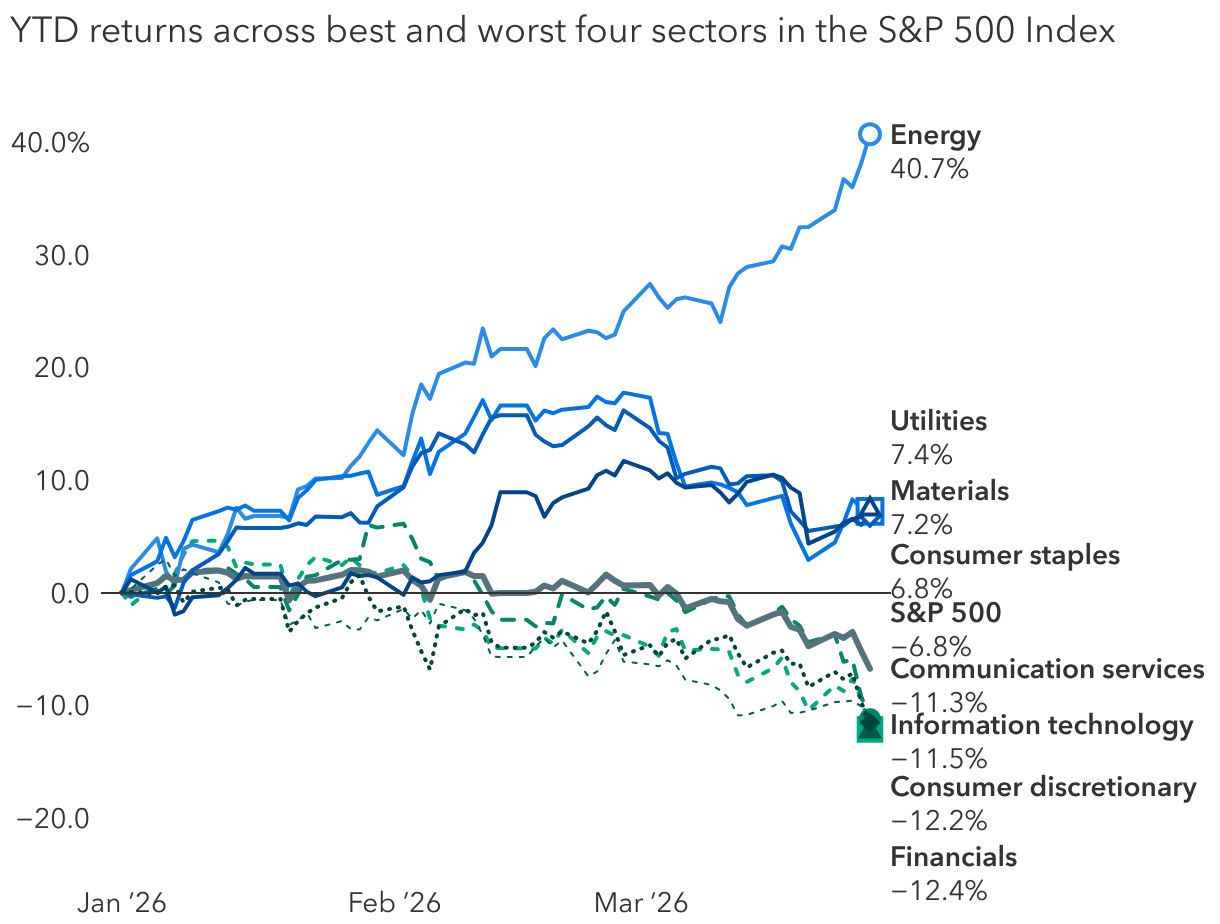

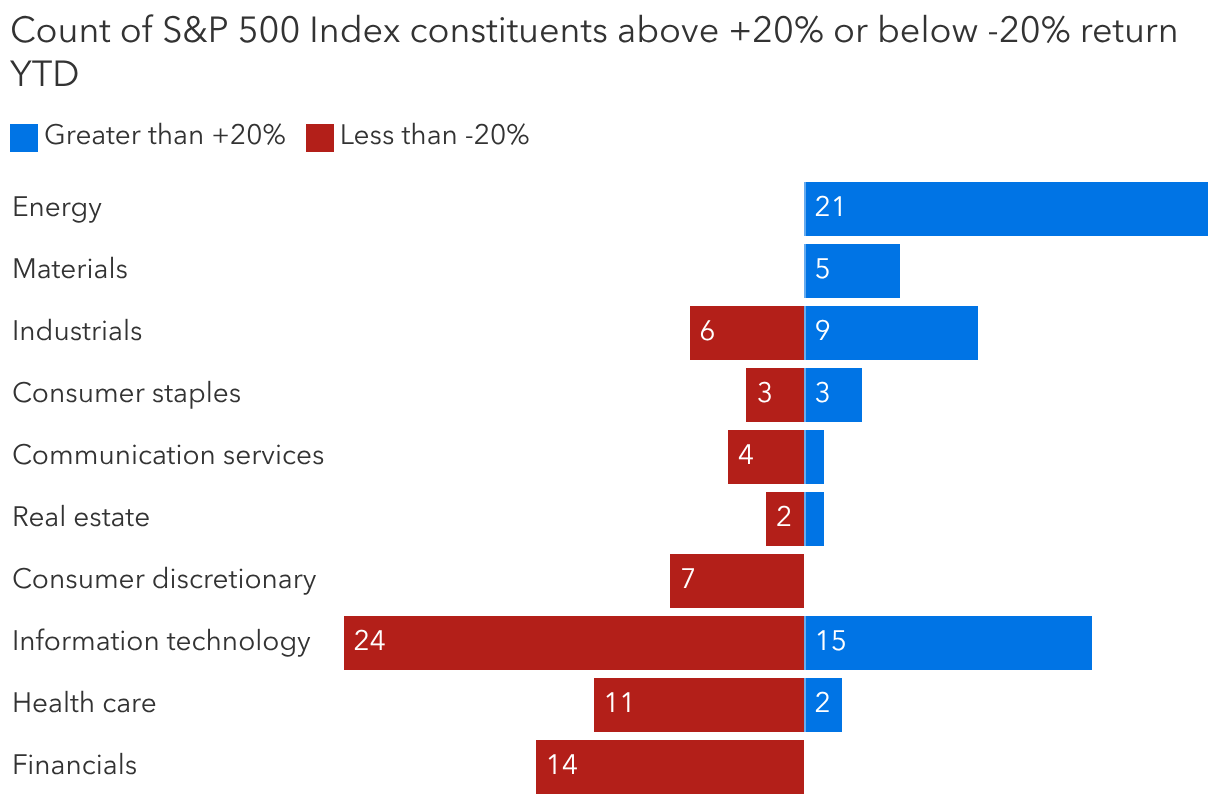

The evolving narrative has driven starkly divergent outcomes for companies. Investors have fled so-called “AI roadkill” — business models such as software that are expected to be rendered obsolete by AI — favoring old economy companies that produce physical goods. Although overall returns for the S&P 500 Index have been negative this year, the energy, materials and industrials sectors have generated solid gains while software and other capital-light industries have suffered sharp declines. Since the start of the Iran war, energy has continued to soar while gains in other asset-heavy industries have moderated.

How should long-term investors think about investing amid these shifts?

“We’re in the early stages of understanding AI’s impact on business models,” explains Brittain Ezzes, portfolio manager for CGDV — Capital Group Dividend Value ETF. “For some it will be highly disruptive. For others it will have a more neutral or even a positive impact. But it would be a mistake to underestimate AI’s potential to reshape the economy.”

As the AI narrative evolves, here are three strategies Ezzes and other members of our investment team are pursuing amid the twists and turns.